Uncategorized

The Annuity Formula for the Present and Future Value of Annuities

This formula is commonly used in corporate finance and banking, but is equally useful in personal or household financial calculations. The effects of compound interest—with compounding periods ranging from daily to annually—may also be included in the formula. Plots are automatically generated to show at a glance how present values could be affected by changes in interest rate, interest period or desired future value.

Calculating Present Value

Bonds are often ordinary annuities because they are paid at the end of a period. Payments are made at the end of every period into an account until the bond matures. An annuity due is the type of annuity that requires a payment at the beginning of a period. You make a payment at the first of each month, and each month thereafter on the same date, until the end of the defined term. Deferred annuities usually earn interest and grow in value, so that to delay the payment by several years increases the payout of the monthly payments. People yet to retire or those that don’t need the money immediately may consider a deferred annuity.

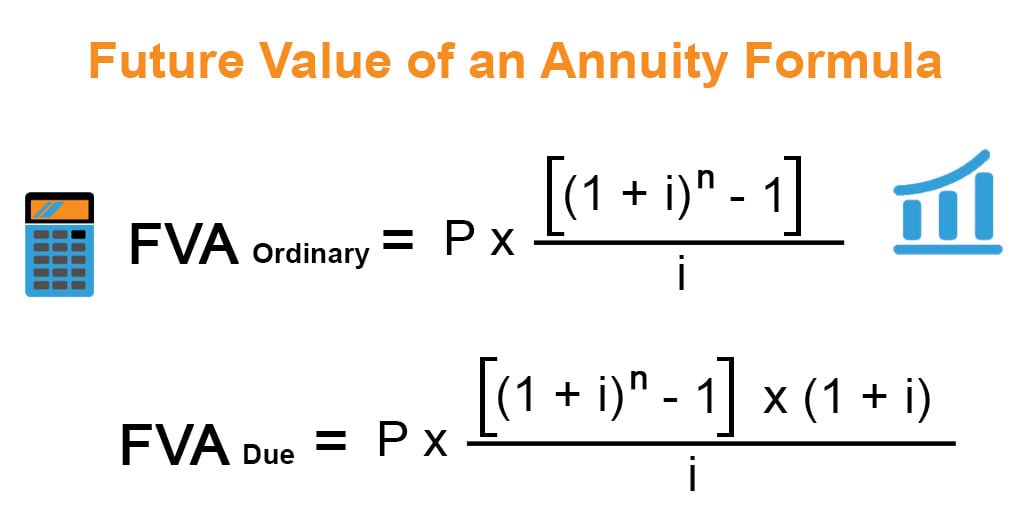

Present Value Annuity Formulas:

However, in practice and in everyday life annuity meaning takes a more explicit form. Buying an annuity usually refers to investment plans, for example insurance products, that provide a steady stream of income in retirement. For example, you can buy an annuity that requires a single upfront payment, or a series of payments to the insurance company. Then, the insurance company pays you either one lump-sum or multiple payments if the insurance pays out. That is the type of payment we will be referring to when calculating the present value of an annuity payment.

Calculating the Present Value of an Annuity Due

The majority of annuity investments are made by investors looking to ensure that they are provided for later in life. It is important for each individual to evaluate their specific situations or consult professionals. This present value calculator can be used to calculate the present value of a certain amount of how big companies won new tax breaks from the trump administration money in the future or periodical annuity payments. The present value of an annuity is the amount of money you will need to pay in order to secure annuity payments in the future. Annuity payments come in many different forms, including annuities that issue a one-time payment, an annual payment, and many others.

- These cash flows will continue for 20 years, at which time you estimate that you can sell the apartment building for $250,000.

- In other words, with this annuity calculator, you can compute the present value of a series of periodic payments to be received at some point in the future.

- With ordinary annuities, payments are made at the end of a specific period.

Treasury bonds are generally considered to be the closest thing to a risk-free investment, so their return is often used for this purpose. An annuity is a financial product that provides a stream of payments to an individual over a period of time, typically in the form of regular installments. Annuities can be either immediate or deferred, depending on when the payments begin. Immediate annuities start paying out right away, while deferred annuities have a delay before payments begin. The present value (PV) of an annuity is the discounted value of the bond’s future payments, adjusted by an appropriate discount rate, which is necessary because of the time value of money (TVM) concept. It is possible to roll over qualified retirement plans like 401(k)s and IRAs into annuities tax-free.

Present Value of an Annuity: Meaning, Formula, and Example

In contrast, MYGAs pay a specific percentage yield for a certain amount of time. MYGAs are a lot like Certificates of Deposit (CDs), except that they have tax deferral benefits, greater time horizons, and are usually purchased with a lump sum of funds. An MYGA’s rate of return is generally similar to that of 10 or 20-year treasury bonds. Investors who can’t decide between investing in a CD or annuity can consider an MYGA. For more information about or to do calculations involving CDs, please visit the CD Calculator.

This can be particularly important when making financial decisions, such as whether to take a lump sum payment from a pension plan or to receive a series of payments from an annuity. Annuities are further differentiated depending on the variability of their cash flows. There are fixed annuities, where the payments are equal, but also variable annuities, that you allow to accumulate and then invest based on several, tax-deferred options. You may also find equity-indexed annuities, where payments are adjusted by an index. The discount rate reflects the time value of money, which means that a dollar today is worth more than a dollar in the future because it can be invested and potentially earn a return. The higher the discount rate, the lower the present value of the annuity, because the future payments are discounted more heavily.

Get instant access to video lessons taught by experienced investment bankers. Learn financial statement modeling, DCF, M&A, LBO, Comps and Excel shortcuts. First, we will calculate the present value (PV) of the annuity given the assumptions regarding the bond. NPV is a key figure in finance, helping to assess the profitability and viability of investments.

Based on your entries, this is the present value of the annuity you entered information for. If you chose to enter a future lump sum, this result represents the periodic payment amount needed to pay off the loan within the specified time period. Commissions–Annuities are generally sold by insurance brokers who charge a fee of anywhere from 1% for the most basic annuity to as much as 10% for complex annuities indexed to the stock market. In general, the simpler the annuity structure or the shorter the surrender charge period, the lower the commission. For example, a variable annuity with a 10-year surrender charge period will pay a higher commission than one with a 5-year surrender charge, which results in a higher commission fee for the investor. In general, commissions for variable annuities average around 4% to 7%, while immediate annuities average from 1% to 3%.